LikeFolio Weekly Roundup

A surprisingly weak jobs report shook the market today. Here's an overview of our biggest movers, including a major win on our SBUX bearish earnings trade and nice move to the upside from our MegaTrends player, RDDT.

Megan Brantley

August 01, 2025

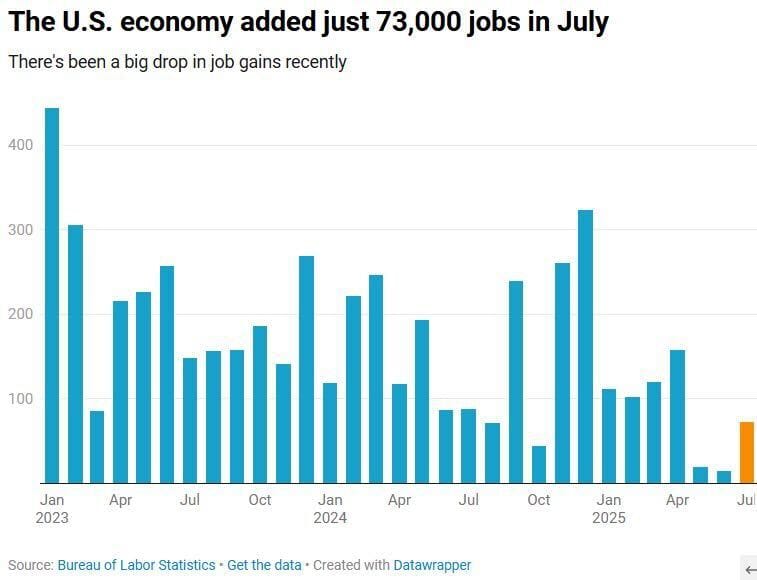

The market opened August with a thud.

The July jobs report landed well below expectations, with the U.S. economy adding just 73,000 jobs, a steep drop from prior months and the slowest print since mid-2022.

June’s figure was revised down sharply to 135,000, and May was lowered as well. That’s two straight months of corrections and a clear sign the labor market is slowing more than previously believed.

That stands in direct contrast to what Fed Chair Jerome Powell said just two days earlier.

On Wednesday, Powell described the job market as still “strong,” with no urgency to cut rates. He warned instead that tariffs might soon push inflation higher. But Friday’s data immediately undercut that narrative. Traders saw it for what it was: a deterioration in labor conditions. Treasury yields dropped across the curve, and the odds of a September rate cut jumped to 76%—from 37% just one day earlier.

The Fed’s stance and the real economy are moving in opposite directions.

And tariff headlines continue to dominate market chatter.

A major U.S.–EU trade agreement signed last week rolls back European tariffs on American industrial goods and opens the door to hundreds of billions in new U.S. energy exports and foreign investment. For sectors like aerospace, oil and gas, and advanced manufacturing, this is a clear win.

Trump’s next wave of duties targeting imports from countries without formal U.S. trade deals takes effect August 7. Markets have been bracing for escalation. But so far, inflation from tariffs has yet to materialize.

Bottom line: All three major indexes are trading lower today, with the Dow, S&P 500, and Nasdaq each pulling back following the weak jobs report and tariff headlines. The Nasdaq is leading declines after recently touching record highs.

This is shaping up like August 2024: a soft summer jobs report, peaking tech valuations, and rising expectations for rate cuts. We said it last week and we will reiterate: August and September can historically be tough months for stocks:

We’re watching for reactions in rate-sensitive names, AI leaders with extended gains, and tariff-exposed sectors as earnings continue next week.

This week, the bearish plays once again dominated earnings – we logged a major win with SBUX, closing out our trade for +95% gains in less than 3 days.

We did catch a nice move to the upside in META, where our data clearly showed AI investments paying off.

Here’s an overview of the biggest news and largest movers in our portfolio through close on Thursday, July 31:

Bitcoin: Bitcoin fell over 3% Friday to the $114K range as traders pulled capital amid tariff-driven volatility and economic slowdown fears. Our conviction remains unchanged. Near-term volatility only serves as accumulation opportunities.

Tesla (TSLA): Tesla slipped alongside broader tech losses, trading in the low‑$300s Friday after Elon Musk confirmed a limited ride-hailing rollout in the Bay Area. The service is operating with safety drivers and doesn’t meet the threshold for full autonomy, undercutting prior expectations for a more aggressive robo-taxi debut. Broader macro pressure from weak jobs data and tariff fears added to the downside, leaving Tesla to drift after a nice run since March-April lows.

Amazon (AMZN): Amazon shares dropped nearly 8%, giving back July gains after a solid Q2 beat was overshadowed by weaker-than-expected profit guidance. Revenue, AWS, and advertising all topped expectations, but investors focused on soft operating income forecasts and AI spending concerns. CEO Andy Jassy defended Amazon’s $100 billion AI investment push but acknowledged rising competition from Microsoft and Google in cloud. AWS growth came in at 18%—well behind Azure and Google Cloud. Jassy also reiterated that tariffs and trade policy remain a wildcard for retail, though so far they haven’t impacted demand. Investors are clearly looking for margin clarity before rewarding top-line strength.

Portfolio Update

RDDT: Up +20% today on Earnings

Reddit surged Friday after delivering a breakout Q2.

Revenue grew 78% year over year to $500 million—its fastest pace in three years—while earnings and guidance both beat estimates. Investor focus was on traction in Reddit Answers, its AI-powered search tool, which grew to 6 million weekly users. Data licensing momentum also accelerated, with $35 million in “other revenue” tied to AI training deals with OpenAI and Google.

Company leadership called Reddit the top domain cited by large language models and pointed to search as a major long-term opportunity. Guidance for Q3 came in well ahead of expectations, flipping the sentiment that weighed on shares earlier this year.

We saw this coming from a mile away. We’ve touched on our bullish-RDDT outlook 7 times since the company’s last report, diving deep into our rationale in a portfolio spotlight in late May.

Reddit ad data continues to improve and we anticipate additional gains from here.

Robinhood (HOOD): Earnings Overview

Robinhood’s 1-year stock chart is nothing short of incredible and proved an extremely high bar ahead of earnings.

Robinhood posted a strong Q2, with earnings doubling and revenue up 45% to $989 million, both well ahead of expectations, but the earnings response was muted.

Options and equities showed solid growth, and crypto volumes jumped 32%, though crypto revenue landed just shy of estimates. Monthly active users rose to 12.8 million year over year, and ARPU hit $151, beating consensus. The quarter included the completed Bitstamp acquisition and early traction in tokenized trading. Shares pulled back slightly, but the core business showed strength across retail engagement, monetization, and platform expansion.

LikeFolio consumer-facing data continues to improve.

Hims & Hers (HIMS): +14%

HIMS shares traded higher this week ahead of next week's earnings, supported by new outcome data from its weight loss program. Customers using compounded GLP-1s reported losing an average of 20.9 pounds in six months with minimal side effects and strong adherence. Only 25% discontinued treatment during that window, compared to typical drop-off rates closer to 80%. The platform also logged more than 6.7 million care team interactions and a 97% improvement rate among customers who completed six-month check-ins. This is an extremely strong nod to customer retention and long-term loyalty.

Aurora Innovation (AUR): -9%

Aurora Innovation delivered its first revenue-generating quarter, reporting $1 million in Q2 sales and launching fully driverless commercial operations between Dallas and Houston. CEO Chris Urmson emphasized that Aurora is no longer selling a concept, but delivering a real product, with over 20,000 safe autonomous miles logged and day-and-night operations already underway. The company confirmed strong liquidity with $1.3 billion in cash, enough to fund operations through 2027, and reaffirmed plans to scale to 10+ trucks by year-end. Despite the operational progress, the stock pulled back following the report as investors weighed a $230 million operating loss and ongoing R&D investment. Management continues to frame 2025 as a capability buildout year, setting the stage for a broader commercial rollout across the Sunbelt in 2026.