Should You Invest in UBER?

We have a better bet on ride-hailing, and if you're a long-term follower of LikeFolio, you can probably guess where we're going with this...

Megan Brantley

October 23, 2025

Uber delivered another strong quarter in August — record trips, 18% revenue growth, and 36 million paid Uber One members — but investors looking several years out face a new question…

Tesla is coming for Uber’s lunch.

The electric automaker’s robotaxi rollout is moving faster than even bullish projections anticipated, its app adoption is already rivaling Uber’s best historical performance, and its next-generation vehicles are laying the groundwork for what could become the largest autonomous fleet on Earth.

Uber’s Current Strength: Scale, Profitability, and Stickiness

Uber reported 3.3 billion trips last quarter, up 18% year over year, with gross bookings of $46.8 billion. Its platform now reaches 180 million monthly active consumers, and profitability per ride improved due to falling insurance costs. For the first time, Uber’s operating income, adjusted EBITDA, and free cash flow all hit record highs.

The company’s membership arm, Uber One, continues to grow rapidly — up 60% last quarter to 36 million paying users. Priced at $9.99 per month or $96 per year, the program offers perks like $0 delivery fees and 5% discounts on eligible rides. Members spend roughly three times as much as non-members, driving recurring, high-margin revenue.

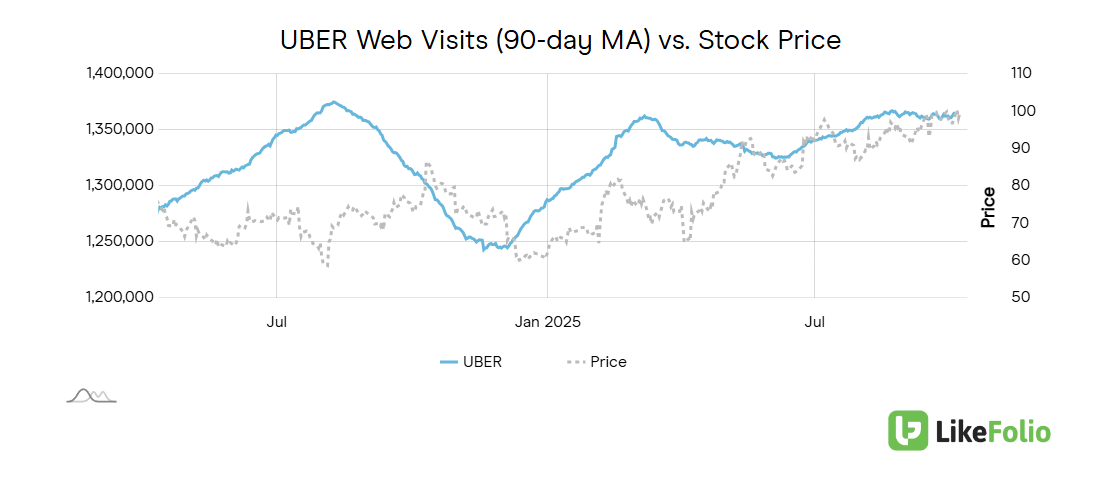

That’s the good news. The concern is that engagement is flattening: LikeFolio data shows Uber’s web visits holding steady since midyear. Meanwhile, Uber Eats is driving growth (+9% YoY in web visits), offsetting softness in rides.

Tesla’s Robotaxi Rollout: The Shockwave No One Priced In

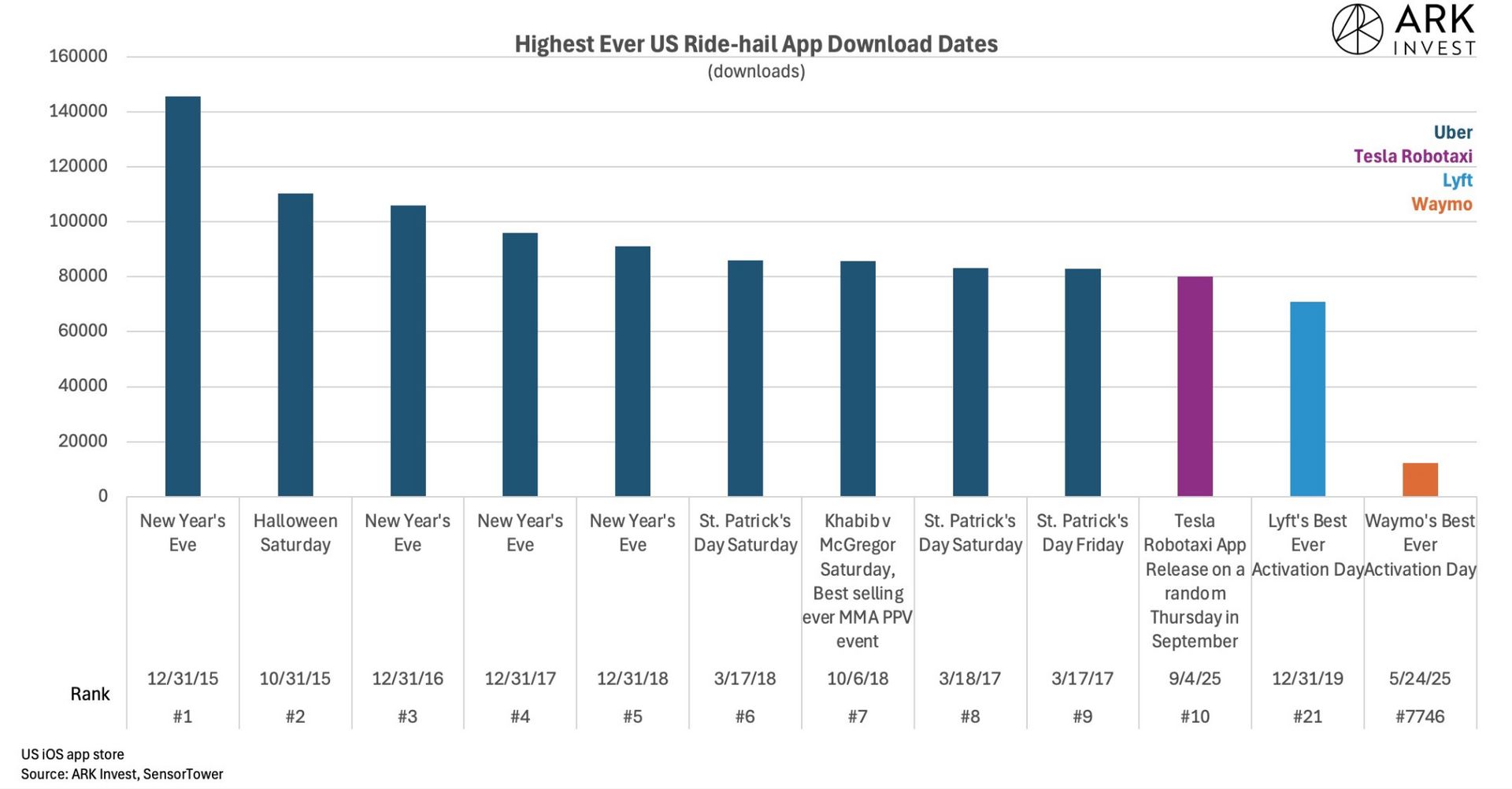

When Tesla launched its Robotaxi app in September 2025, it wasn’t on a holiday or during an event weekend, it was a random Thursday. Yet the app’s debut ranked among the top 10 ride-hail app download days in U.S. history, per ARK Invest’s SensorTower analysis.

Uber’s biggest download spikes came on predictable nights like New Year’s Eve or Halloween — Tesla matched those numbers with zero lead-up.

Lyft’s best activation day ranks #21. Waymo’s? #7746.

That single data point should rattle every rideshare investor: consumer loyalty doesn’t exist in ride-hailing.

When Tesla offered a cleaner interface, seamless app setup, and a lower price, consumers jumped instantly.

Tesla’s first-day app downloads nearly hit Uber’s average daily peak from its hyper-growth years. In a single day, Tesla proved what took Uber years to build: the audience is already there, waiting for a cheaper, automated alternative.

Tesla’s Cost Advantage: A Gap That Can’t Be Ignored

Tesla’s early rollout in Austin revealed what Uber executives dread: a radically lower cost structure.

Rides began with $4.20 flat fares, later shifting to dynamic pricing averaging $1.25 per mile, versus Uber’s $2.00+ per mile for comparable trips.

That’s a 40–70% cost advantage with no driver commissions, no tips, and no surge markups.

Behind that pricing power is Tesla’s vertical integration. Every part of the stack, vehicle, battery, software, network, is in-house. The company is now shipping Model 3 and Model Y trims equipped with Full Self-Driving hardware, effectively seeding a robotaxi-ready fleet into global circulation.

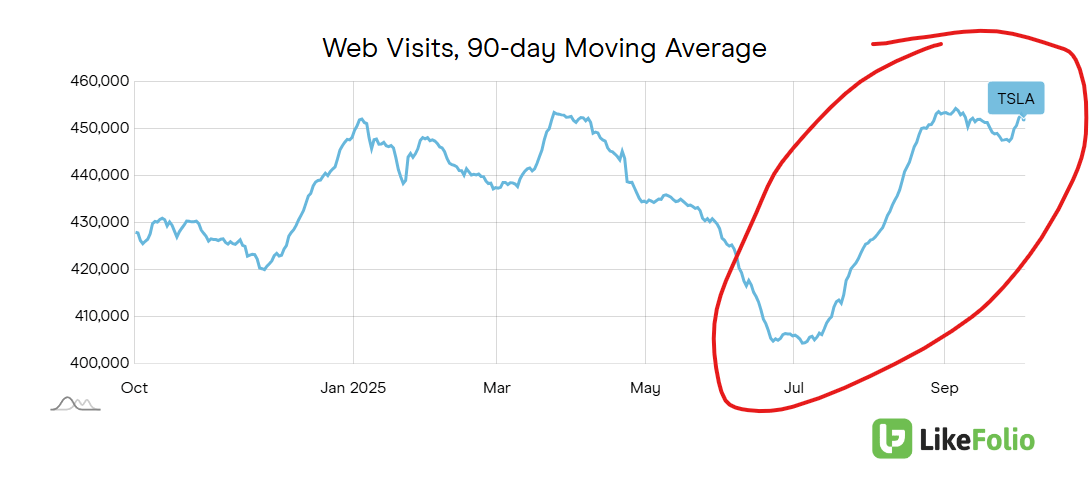

Tesla vehicle demand surged over the last quarter:

Next comes the Cybercab, a fully autonomous, no-steering-wheel vehicle optimized for fleet use, expected to enter production before 2027. Combine that with Tesla’s plan to allow owners to list their vehicles on the Tesla Network, and the potential supply explosion becomes clear.

Tesla could activate hundreds of thousands of cars overnight — no new manufacturing required.

Uber’s AV Strategy: Safe, Profitable, but Slow

Uber is doing what Wall Street loves: maintaining profitability while “partnering” into autonomy.

It’s aligning with Waymo, Nuro, and Lucid to bring autonomous rides to market, an asset-light approach that minimizes risk but also cedes control. CEO Dara Khosrowshahi acknowledged that Tesla’s rollout is “very small for now” but admitted that hardware, not software, will determine scalability. That’s exactly where Tesla already leads.

Uber’s model depends on blending human and autonomous supply — a fine strategy in the short term, but one that could be structurally disadvantaged against Tesla’s direct-to-consumer, vertically owned system.