The Ad War No One Saw Coming...

For years we've talked about streaming vs. linear ad spend. Now, a new player is entering the chat and it's shaking things up in a big way. Here's the top stocks to keep an eye on.

Megan Brantley

November 04, 2025

The streaming boom isn’t dead, but the easy ad money is.

And it’s creating a growing divide of winners and losers in an industry that was once a story of a rising tide lifting all boats.

Look at this chart.

It shows the share of U.S. streaming TV time since 2022. YouTube’s line in red keeps climbing, while Netflix’s line in blue has been trending lower.

This is a warning for advertisers and investors.

Consumers are spending more time with platforms that mix premium shows, live sports, and user-generated content.

That change in viewing habits may be the early sign of a broader shift in how streaming time and ad budgets get distributed.

Netflix’s most recent quarter showed how this can play out in the stock market.

The company reported $11.5B in revenue, up 17% YoY, and $2.7B in free cash flow. Paid memberships rose 12%. Yet inside those solid results was a slowdown that matters: ad revenue is not scaling as quickly as expected. And the stock sold off.

Management called ad sales “record” and said ad revenue will “roughly double” in 2025, but it did not share any actual numbers. For a business that was supposed to ignite the next phase of growth, that silence is telling.

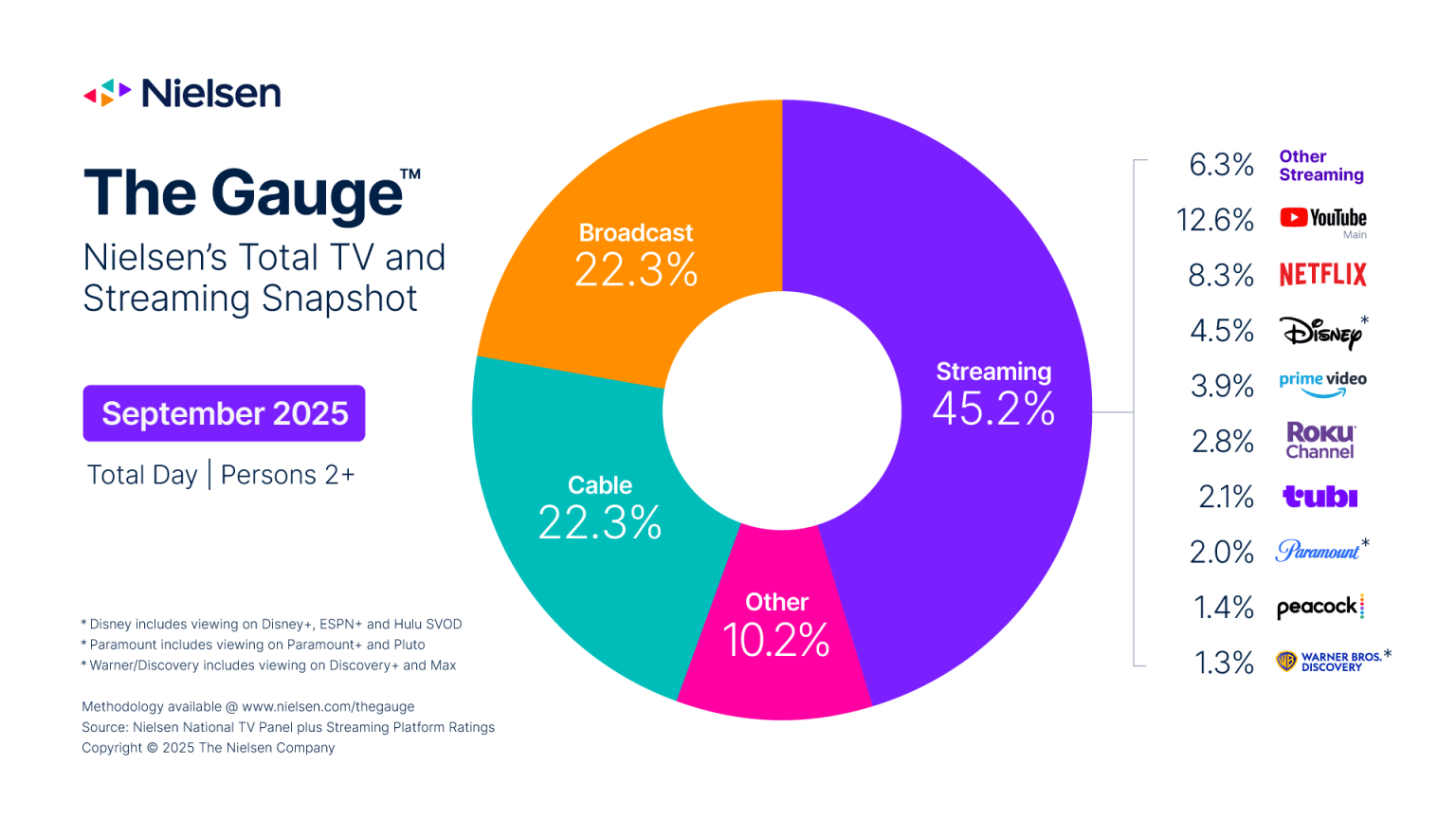

To be clear: streaming still commands more eyeballs than broadcast and cable combined, according to Nielsen’s streaming snapshot from September.

But the pace of new ad spending is slowing.

The early surge of connected-TV experimentation has given way to tighter budgets and a preference for platforms that can target audiences with greater accuracy…like these:

Alphabet (GOOGL) captures that demand. YouTube now represents about 12.6% of total U.S. television viewing, the largest share held by any single platform across broadcast, cable, or streaming. In Q3 2025, YouTube ad sales reached approximately $10.2 billion, up ~15% YoY, as advertisers consolidate spend around scalable video inventory inside Google Ads — and GOOGL shares soared post report.

Amazon (AMZN) links entertainment and commerce. Prime Video’s ad tier, launched in early 2025, now reaches over 130 million monthly viewers globally, and Freevee extends that footprint across free, ad-supported streaming. In Q3 2025, Amazon’s advertising services revenue was about $17.7 billion, up ~24% YoY, flexing ongoing strength in retail-media integrations that connect viewing data directly to product sales.

Meta (META) is positioned to capture share as brand dollars slow their expansion into connected TV and consolidate around global video platforms. In Q3 2025, Meta reported $50.1 billion in advertising revenue, up 26% YoY. Reels continues to dominate user time, now accounting for a majority of time spent on Instagram, giving Meta’s video formats a reach and engagement depth that rival streaming platforms without the same content-production costs.

Reddit (RDDT) is gaining traction as a complementary video and conversation platform. Reddit shares surged last week after the company reported revenue of $585 million, up ~68% YoY, supported by higher video engagement and brand-campaign demand. With approximately 116 million daily active users, Reddit gives advertisers access to entertainment-adjacent communities that are implicitly niche in nature. These results “speak to the company’s continued progress across its ad and platform initiatives,” wrote Morgan Stanley — we agree.

Meanwhile, Netflix’s ad growth ambiguity exposes pressure on companies most reliant on streaming ad cycles:

Roku (ROKU), The Trade Desk (TTD), and Magnite (MGNI) depend on rising connected-TV budgets. Roku controls the home screen, The Trade Desk connects buyers and streamers programmatically, and Magnite handles the supply side.

If Netflix cannot accelerate ad revenue despite its global scale, it implies that the wider CTV market is progressing more gradually than expected.

Roku’s ad yield improves when budgets expand.

The Trade Desk benefits when programmatic video spending rises.

Magnite’s growth depends on fill rates and pricing.

A cautious ad environment slows all three.

These companies still hold long-term relevance, but the near-term setup is tougher. The open-internet ecosystem now competes with data-rich closed platforms that can offer advertisers precise targeting and buy-now features today.

Disney (DIS) remains the key exception among traditional streamers, with its Hulu and Disney+ ad tiers continuing to draw brand demand through premium sports and bundled reach, which have consistently brought ad dollars to the table.

But ALL of the stocks previously mentioned are in imminent competition for ad dollars from a player that didn’t even exist a few years ago: Artificial Intelligence.

The Emerging Elephant in the Room: AI Shopping

AI-driven shopping is opening a new front in the competition for ad budgets. It does not erase traditional advertising, but it introduces a channel where discovery, recommendation, and purchase all happen inside one interaction. That dynamic could reshape how marketers divide spending across search, social, and streaming.

Adobe recorded a 4,700% YoY increase in referrals to product pages from AI chatbots in July, a clear sign that shoppers are beginning to trust conversational tools for product discovery.

ChatGPT now reaches about 700M weekly active users, and BofA estimates roughly 20B shopping-related messages this year. Each of those exchanges represents an opportunity that previously belonged to Google search ads, Meta feed placements, or connected TV brand campaigns.

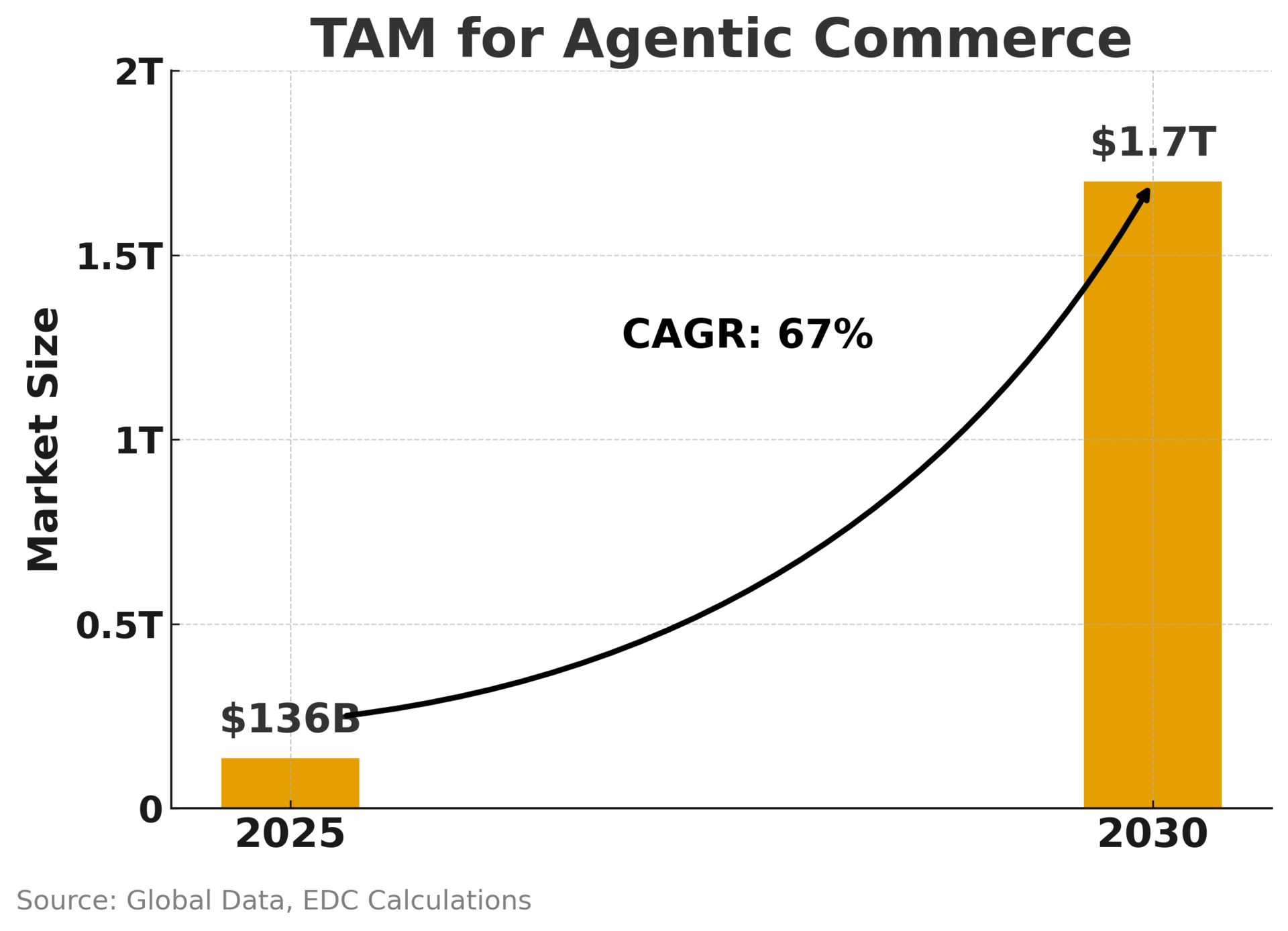

OpenAI announced its Instant Checkout and Agentic Commerce Protocol on September 29, 2025, with U.S. rollout to begin in November. Users will be able to buy products directly through ChatGPT via Etsy, with Shopify integration next. That announcement sent Etsy stock up 16% and Shopify up 6%, after both companies were confirmed as launch partners for the new shopping tools. Consultancy Edgar, Dunn & Co. projects $136B in agent-initiated transactions in 2025, rising to $1.7T by 2030, a figure that would rival today’s global retail media market.

Major platforms are preparing accordingly. Amazon’s Rufus assistant is testing automated “Buy For Me” features that keep purchases within its ecosystem. Walmart’s Sparky tool learns user budgets and preferences to deliver personalized shopping suggestions. Google’s Gemini chatbot integrates sponsored try-ons and price tracking inside AI Overviews. Meta plans to extend its ad targeting to conversations with Meta AI later this year.

The payments layer is forming beneath it all. Google, PayPal, and Mastercard are building an agent-payment protocol. OpenAI is partnering with Stripe, while Visa and Affirm are developing systems for AI-enabled checkout. Once those connections mature, advertisers will be able to track engagement and conversion in a single, high-intent environment.

For marketers, this creates a new precision channel competing directly with search, social, and connected TV for the same dollars.

Budgets will flow toward whatever medium connects intent to purchase most efficiently.

Streaming remains dominant for attention, but AI shopping is quickly emerging as the next major destination for performance-driven spend.

Bottom Line

Streaming still wins the living room, but the easy ad money phase is over. Netflix’s quarter made clear that future growth depends on owning the connection between what people watch and what they buy.

Near-term, AI shopping is poised to build that bridge faster. Chatbots and LLMs are no longer a novelty, they are a storefront. As consumers start asking AI assistants what to watch, wear, and order, the dollars that once powered connected TV will follow them.

The next big fight for ad budgets isn’t streaming vs. linear TV — instead it will happen inside AI platforms where consumer purchase intent turns into action in real time. Streaming owns attention, but AI is beginning to own the transaction.

We’re watching this MegaTrend very closely…